In ancient times, the Roman poet Horace coined the phrase, “carpe diem,” which translates to “seize the day.” Little did he know that his wise advice would help 21st century plan participants successfully prepare for retirement.

History shows us that the most important ingredient for long-term investing is to save as much as you can today. It is plan contributions that have the largest impact on outcomes. Contribution decisions–in particular, the use of automatic enrollment and automatic escalation for employee deferrals, the size of employer contributions, and the total produced by both–are in the end more influential in driving retirement security.

Of course, in thinking about improving participant outcomes, investment committees rightly spend a great deal of time on the construction of a defined contribution (DC) investment lineup. This includes the structure of the investment menu, the types of strategies and managers offered, the selection of a default investment (when relevant), and fees paid. As we noted in our paper, Constructing a defined contribution investment lineup: Four best practices, the paradigm for making such choices has changed in DC plans. Sponsors have emerged as “choice architects,” balancing the need for a well-designed default fund affecting many participants, against the expanded menu options for a minority of participants wanting to make active investment choices. But while investment evaluation and menu design remain critical plan sponsor duties, their ability to increase participant savings rates is essential.

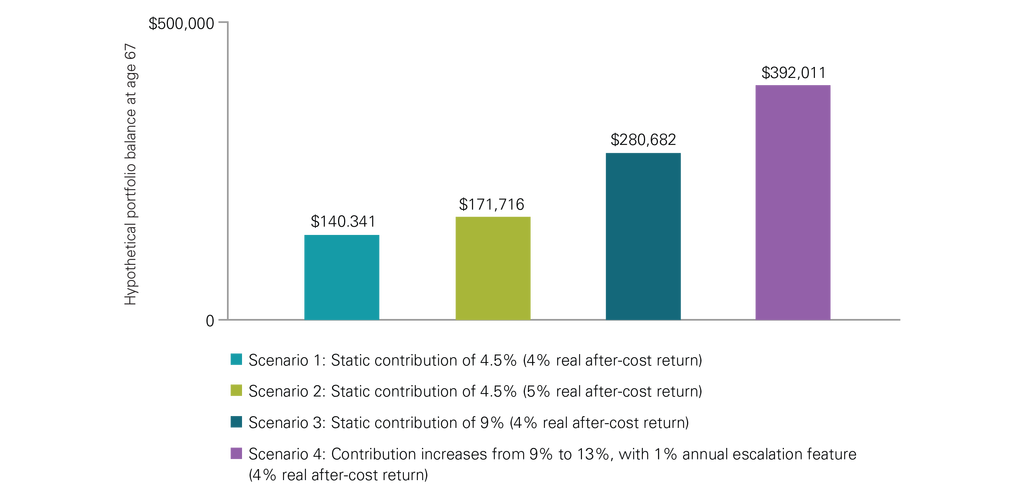

To illustrate this point, consider four different hypothetical scenarios involving a young participant saving over a working career, with standard demographic and plan design assumptions.¹

In the first scenario, the participant is automatically enrolled at 3% of pay, earns an employer match of 1.5% of pay, for a total contribution rate of 4.5% per year. Real investment returns net of fees are 4%. Our participant is projected to retire with a little more than $140,000.

In the second scenario, all details are the same—except real net returns are higher, at 5% per year after costs. That gives a meaningful boost to retirement savings, which reach close to $172,000. But to take on those returns, the participant must assume higher risk—a fact not captured in this simple illustration.

But in the third and fourth scenarios, the participant earns a net real return of 4%, but contribution rates are much higher. In scenario three, the participant’s total contribution is double, at 9% of pay (assuming auto enrollment at 6% with a 3% employer match). And, in scenario four, the total contribution rate is 13% (assuming an escalation feature of 1% from 6% to 10% in the early years). In these latter cases, savings at retirement is now either $280,000 or $392,000. That’s double or nearly triple the savings from the first scenario.

Higher contribution rates lead to better outcomes

These results underscore how important contribution rates, not relative investment returns, are in determining retirement outcomes. On the investment side of the equation, the sponsor can control asset allocation (of the overall menu and the default fund) and investment fees, but not the equity risk premium. Contributions are directly under sponsors’ control, particularly with the growing use of automatic enrollment and automatic escalation, and the important influence of inertia in participant decision-making.

Can an employer-sponsored DC plan be certain to provide retirement security? No, not in a world of uncertain market returns. But can employers substantially improve the odds of great retirement outcomes through a well-designed policy on plan contributions? As the data shows, the answer is a definite yes. Make sure that your employees seize the day now to achieve a better tomorrow.

I’d like to thank my colleague Frank Chism in Vanguard’s Investment Strategy Group for his contributions to this piece.

¹ The key demographic assumptions: The participant has a starting salary of $35,000, earns 1% real wage increases per year, joins his or her DC retirement plan at age 32, and contributes for 35 years until age 67. The employer offers a $0.50 on the dollar match up to 6% of pay. These hypothetical examples do not represent the return on any particular investment and the rate is not guaranteed. The final account balance does not reflect any taxes or penalties that may be due upon distribution. Withdrawals from a tax-deferred plan before age 59½ are subject to a 10% federal penalty tax unless an exception applies.

Note: All investing is subject to risk, including the possible loss of the money you invest.

About Steve Utkus

Mr. Utkus is principal and director of the Vanguard Center for Investor Research. The Center conducts and sponsors research on investor behavior and decision-making. It also works to apply behavioral insights to real-world settings. The Center’s scope includes individual investors (whether direct, advised, or in defined contribution plans) and institutional investors. The Center’s work will be of interest to investors, advisors, consultants, employers, media, the research community, and policymakers. Mr. Utkus’s personal research interests include retirement economics, behavioral finance, and the role of psychology in household financial decisions. He earned a B.S. from the Massachusetts Institute of Technology and an M.B.A. from The Wharton School of the University of Pennsylvania. He is a member of the advisory board of the Wharton Pension Research Council, is currently a visiting scholar at Wharton, and is a member of the board of trustees of the Employee Benefit Research Institute in Washington, D.C.